Stamp duty second homes UK is a key cost that many buyers underestimate. When you buy an additional property, the tax rules change. Therefore, the total cost becomes higher compared to buying your first home.

How stamp duty second homes UK works

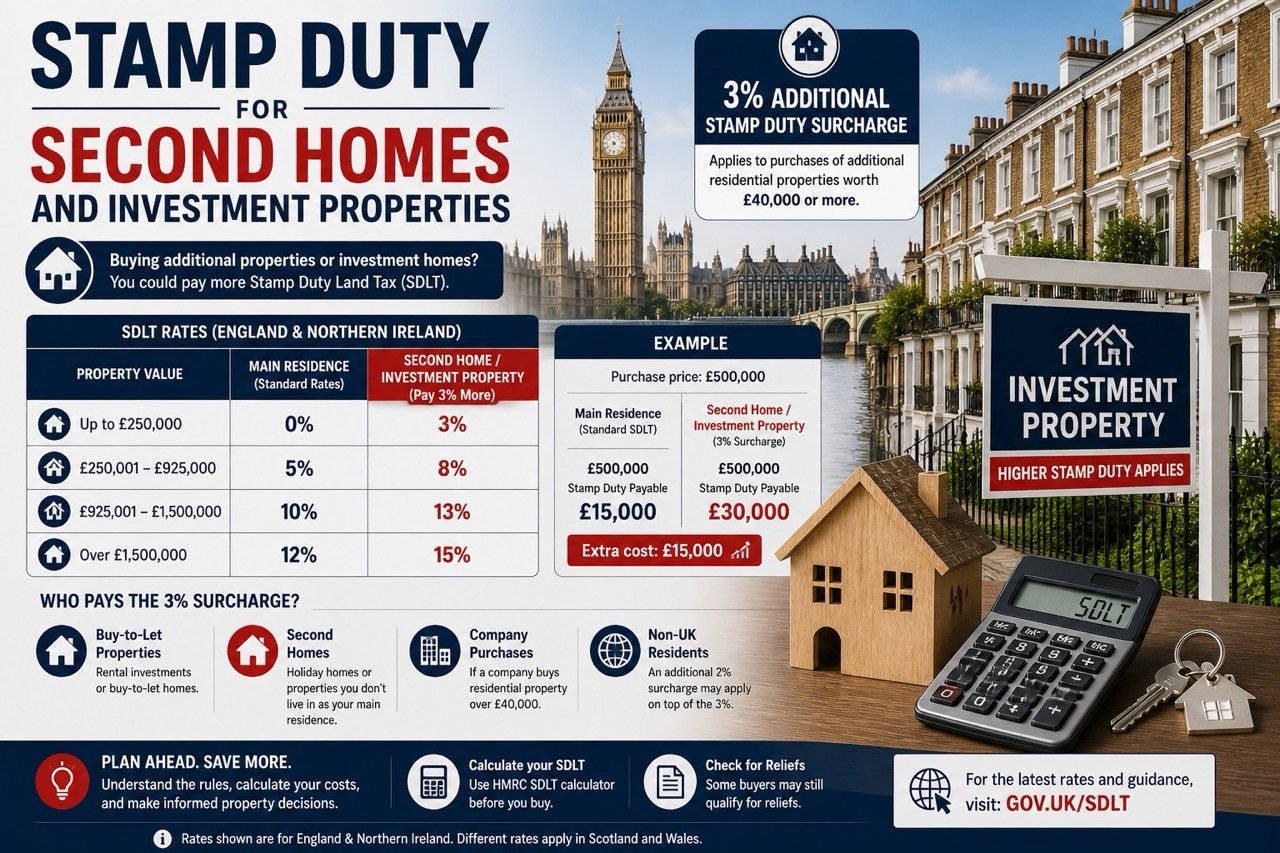

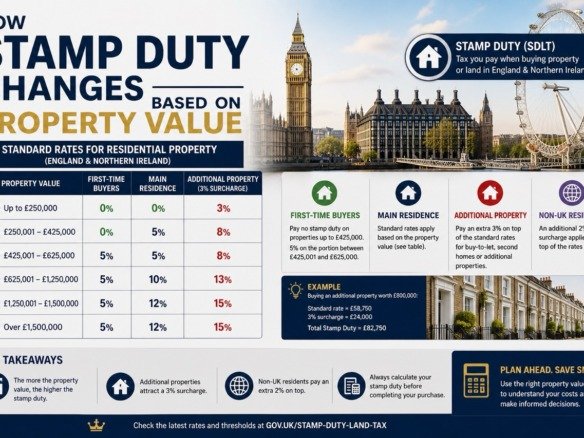

Stamp duty applies to most property purchases. However, second homes and investment properties usually include an extra surcharge. Because of this, buyers pay more than standard rates.

In addition, this surcharge applies on top of normal stamp duty bands. Therefore, the total tax increases across the entire property value.

Buyers who review UK housing supply and demand statistics often understand how these costs impact investment decisions.

Why second homes have higher stamp duty

Additional property surcharge

If you already own a property, buying another one triggers an extra tax rate. Therefore, investors and second home buyers pay more.

Because of this, total purchase costs can rise significantly.

Many buyers explore property for sale in London to compare investment opportunities after calculating tax.

Buy to let properties

Investment properties are also subject to higher rates. Therefore, landlords must include stamp duty in their financial planning.

In addition, rental income should be analysed carefully. Because of this, investors focus on long term returns.

Stamp duty second homes UK and property value

Price bands still apply

Stamp duty still works in bands. However, the additional surcharge increases the tax in each band.

Because of this, higher value properties lead to even larger tax payments.

Impact on total investment

Stamp duty becomes a major part of the total investment. Therefore, buyers must calculate full costs before buying.

Buyers often review London property price trends and data to understand how pricing affects returns.

Financial considerations for second home buyers

Interest rates and financing

Interest rates affect investment returns. Therefore, higher borrowing costs can reduce profitability.

Because of this, investors monitor UK interest rates and mortgage updates closely.

Long term vs short term returns

Stamp duty is an upfront cost. However, long term growth and rental income can offset it.

Therefore, investors should focus on long term strategy instead of short term costs.

How to manage stamp duty second homes UK

Plan your purchase carefully

Understanding tax rules helps reduce risk. Therefore, planning ahead is essential.

Because of this, buyers can make better financial decisions.

Consider timing and strategy

Market conditions can influence your purchase. Therefore, timing may affect overall costs.

Buyers who research when is the best time to buy off plan property often improve their investment strategy.

Compare multiple options

Comparing properties helps identify better opportunities. Therefore, investors can choose the most efficient option.

Reviewing search results for London properties helps compare prices and total investment costs.

Common mistakes investors make

Ignoring extra costs

Many investors focus only on property price. However, stamp duty and other costs increase the total investment.

Because of this, returns may be lower than expected.

Not planning long term

Short term thinking can lead to poor decisions. Therefore, investors should focus on long term growth.

Because of this, they can recover upfront costs over time.

Final thoughts on stamp duty second homes UK

Stamp duty second homes UK is a major factor in property investment. It increases costs but should not discourage investors.

Therefore, understanding how it works helps you plan better.

Because of this, informed investors can manage costs and achieve stronger returns.

Join The Discussion